The mood I am getting from the media this weekend is by no means sanguine. I thought I would start on the issue of China and its effect on the global economy. There is constant mention of the fact that China’s economy may not be as stable as economists and commentators had thought. The past decade has seen annual growth in the region of 10%. Despite what appears to be good management of the economy, there is doubt surrounding how effective the Chinese government will be in the years going forward.

Developments stand vacant throughout China

The Chinese introduced a hefty credit stimulus package into their banking system in 2008, which certainly did not help with rising inflation. As with many Western governments, it is yet to be seen how the Chinese will deal with inflationary pressure in the years to come. Around 60% of the Chinese GDP can be attributed to the construction sector, which received much of the capital that was injected into the economy.

With endless buildings being constructed in towns that are yet to be occupied, I am reminded about Dubai and the 25% - 50% plus falls that were seen in property prices a few years back as demand for property fell. This does not bode well for development demand in China over the years to come. I say this because much of this development has been forward thinking, providing room for a lag in growth in the shorter term. This brings the global economy into play, as overall demand dwindles as we move towards 2012.

The big question is whether Western efforts to prevent the likely double dip will be in vain. The West remains to be China’s biggest customer, which poses much risk to China in the event of further stagnation over here. Europe and America are less likely to prop up Chinese industry as demand for goods declines. It can be seen here how having interlinked economies poses a threat to global demand across many sectors. And property is by no means the asset class of choice for many individuals and/or investors after a decade of healthy growth.

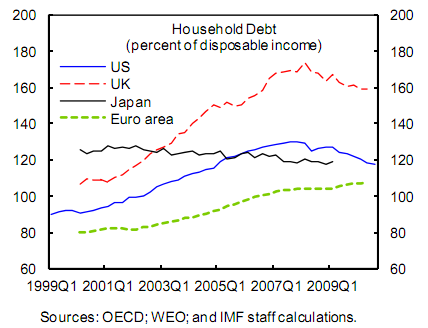

The consensus I am getting from the internet is that many people are reverting to a more aggressive approach to managing debt. As people save up to tackle their household debt there will be further reduction in consumption, stifling economies in the short to medium term. Whether or not house prices will take a further hit is yet to be seen. However, I would expect a price correction in one form or another. This may take the form of prolonged stagnant growth, or more immediate devaluations that rebalance the market.

The overall effect of slowing demand should cause property prices to decline as sentiment worsens and people are less willing to take on debt to make acquisitions. In fact, recent data shows that Brits have the highest debt to disposable income ratio in the world. Many consumers will have to tighten their belts in order to plan ahead and manage their exposure to debt.

{kind=link}

|

| UK National House Prices: 2002 - 2011 |

During the bulk of 2008 and part of 2009, the UK experienced falls in house prices of circa 10% in most cases as seen in the graph above. Since then average house price growth has been negligible, with near 2006 levels being seen at present. Inflation in the UK is on the up and has breached 5%, raising concerns over its trajectory.

Inflation has the effect of eroding peoples’ disposable income and is likely to have a negative effect on real house price growth for some time to come. Inflation and rising unemployment, coupled with high indebtedness and fears of the “double dip recession”, have only served to hamper sentiment in the property market and will continue to create further downward pressure on prices.

On the flipside, it remains possible for short term growth to be in line with credit expansion. However, this cannot continue indefinitely as the market calls for correction. Fortunately for homeowners in more metropolitan areas in the UK, there still remains a supply shortage in relation to projected population growth. While we have seen improved data in the construction sector for the year, supply will remain tight as a result of a growing population.

One important point to note here is the movement of students and professionals from the EU into the UK as a result of instability in the Eurozone. Many university cities are experiencing growing numbers of applicants from the UK and abroad. London in particular receives the bulk of working immigrants as job prospects dwindle in their home countries. This raises rents in the areas concerned which will have the effect of pushing rental yields up, which in turn supports property prices. While this may work in a low interest rate environment, it is yet to be seen how the market evolves as rates rise.

While there is much debate about the direction of the UK property market, there is better consensus among commentators on the US market as we see continued vulnerability in this sector.

Uploaded by nsotd4 on 4 Oct 2011

UK housing market in crisis with Housing Minister Grant Shapps

Published on 30 Aug 2011 by itnnews

{kind=link}

Inflation has the effect of eroding peoples’ disposable income and is likely to have a negative effect on real house price growth for some time to come. Inflation and rising unemployment, coupled with high indebtedness and fears of the “double dip recession”, have only served to hamper sentiment in the property market and will continue to create further downward pressure on prices.

On the flipside, it remains possible for short term growth to be in line with credit expansion. However, this cannot continue indefinitely as the market calls for correction. Fortunately for homeowners in more metropolitan areas in the UK, there still remains a supply shortage in relation to projected population growth. While we have seen improved data in the construction sector for the year, supply will remain tight as a result of a growing population.

One important point to note here is the movement of students and professionals from the EU into the UK as a result of instability in the Eurozone. Many university cities are experiencing growing numbers of applicants from the UK and abroad. London in particular receives the bulk of working immigrants as job prospects dwindle in their home countries. This raises rents in the areas concerned which will have the effect of pushing rental yields up, which in turn supports property prices. While this may work in a low interest rate environment, it is yet to be seen how the market evolves as rates rise.

While there is much debate about the direction of the UK property market, there is better consensus among commentators on the US market as we see continued vulnerability in this sector.

IMF advisor says we face a Worldwide Banking Meltdown: 05/10/11

Uploaded by nsotd4 on 5 Oct 2011

Former Bank of England Economist says we face no growth 10 years: 04/10/2011

UK housing market in crisis with Housing Minister Grant Shapps

Published on 30 Aug 2011 by itnnews

UK Housing Market: A Safe Investment?

Uploaded by CranfieldSoM on 29 Oct 2010

Uploaded by CranfieldSoM on 29 Oct 2010

London and UK property markets - where is safe?Uploaded by cantosTV on 28 Jul 2008

Here Liam Bailey at Knight Frank discusses the dynamics of the London market going forward from 2008. He also covers issues of supply and demand in the UK and London as well as mainstream, prime and super prime markets.

Relevant Video Links:

Bloomberg: Decline in U.K. House Prices to Accelerate 03/10/2011

Gardner Says U.K. House Prices May Move `Slightly Lower' 29/09/2011

Another thing to look at is this new proposed EU Financial tax. This tax would raise approx. 45 Billion Euro a year by doing the following: The European tax would levy trades in shares and bonds at a rate of 0.1pc and derivative contracts at a rate of 0.01pc from Jan 2014.

ReplyDeleteHowever, this is tax would be not proportionate in that 80 % of the tax receipts would come from London's financial sector! Basically surmounting this tax to a EU Tax on the UK for the direct benefit of the Euro Zone and not the UK economy.

Fortunately, this tax cannot be levied on the UK without the UK governments consent (they have the right to veto the tax).

But this attempt by the EU executive coupled with the EU also attempting to force the UK government to give EU nationals social benefits without question and thus qualification is worrying. It would seem the EU is attempting to impose itself on the UK in a indirect manner to bolster the coffers of Euro Zone countries. This can only back fire as this will be fiercely resisted by the UK government and only strain ties within the EU.